Why a Modern Multi-Chain Wallet Changes How You Own Crypto

Whoa!

I still remember the first time I watched a DEX trade fail because of a gas spike. It was frustrating and oddly educational. My gut said something felt off about trusting a single chain for everything. Initially I thought a single wallet per chain would suffice, but then I realized that fragmentation kills both usability and security if you let it. On one hand convenience matters, though actually security and transparency matter more when money is on the line.

Seriously?

Yes, seriously—multi-chain is not marketing fluff. The technical reality is that users increasingly spread assets across Ethereum, BSC, Polygon, Avalanche and a half-dozen EVM compatibles. A good wallet needs to present that spread as one coherent portfolio, not as a set of islands. My instinct said the UX has to be simple because most users don’t want to manage ten seed phrases. So the design challenge becomes: unify without centralizing trust.

Hmm…

Here’s the thing. People ask me often whether a wallet that simulates transactions is overkill. I tend to reply with a short anecdote: I once almost sent a token that looked legit but was actually a scam copy, and a good simulator would have flagged the malicious approval flow. The more I dug into transaction previews and static analysis, the more I saw their value for everyday DeFi interactions. In practice, simulation reduces costly mistakes in a way that education alone rarely does.

Okay, check this out—

Wallets today must do more than hold keys. They need to simulate swaps, preview approvals, and surface risks before you hit confirm. That preview step is the single most underused defense against rug pulls and phishing approvals. I’m biased, but having used several wallets, the ones that integrate robust simulation feel like they save me time and money. Also, the UX of transaction simulation matters—if it’s clunky people ignore it, which is a bummer.

Wow!

Portfolio tracking is about mental models as much as math. A clear net worth view across chains helps people make better decisions and avoid panic selling during volatile periods. I noticed that when I could see my tokens aggregated, I made fewer impulsive moves. On the flip side, overaggregation can hide chain-specific nuances like bridging fees or staking locks, so a wallet needs to surface those exceptions gracefully. Balance matters; show the total, but let users zoom into the specifics.

Really?

Yes—security features must be visible, not hidden. Multi-chain wallets should adopt layered security: hardware-compatible key management, transaction simulation, granular approval controls, and clear ability to revoke permissions. There’s a trend toward smart transaction guards that automatically block risky flows, and that trend is good. I’ll be honest—some of this tech still feels early, and guard rules can produce false positives that annoy power users. But overall the direction is right: proactive defense beats reactive panic.

Whoa!

Let me be practical: wallet ergonomics change adoption. If a wallet makes bridging feel like mailing a letter, people use it. That analogy is a little loose, but you get it—simplicity lowers cognitive load. Building intuitive flows for cross-chain swaps and showing estimated final balances after fees is very very important. Oh, and by the way, transaction cost estimation needs to show gas in fiat terms, otherwise users misjudge impact.

Hmm…

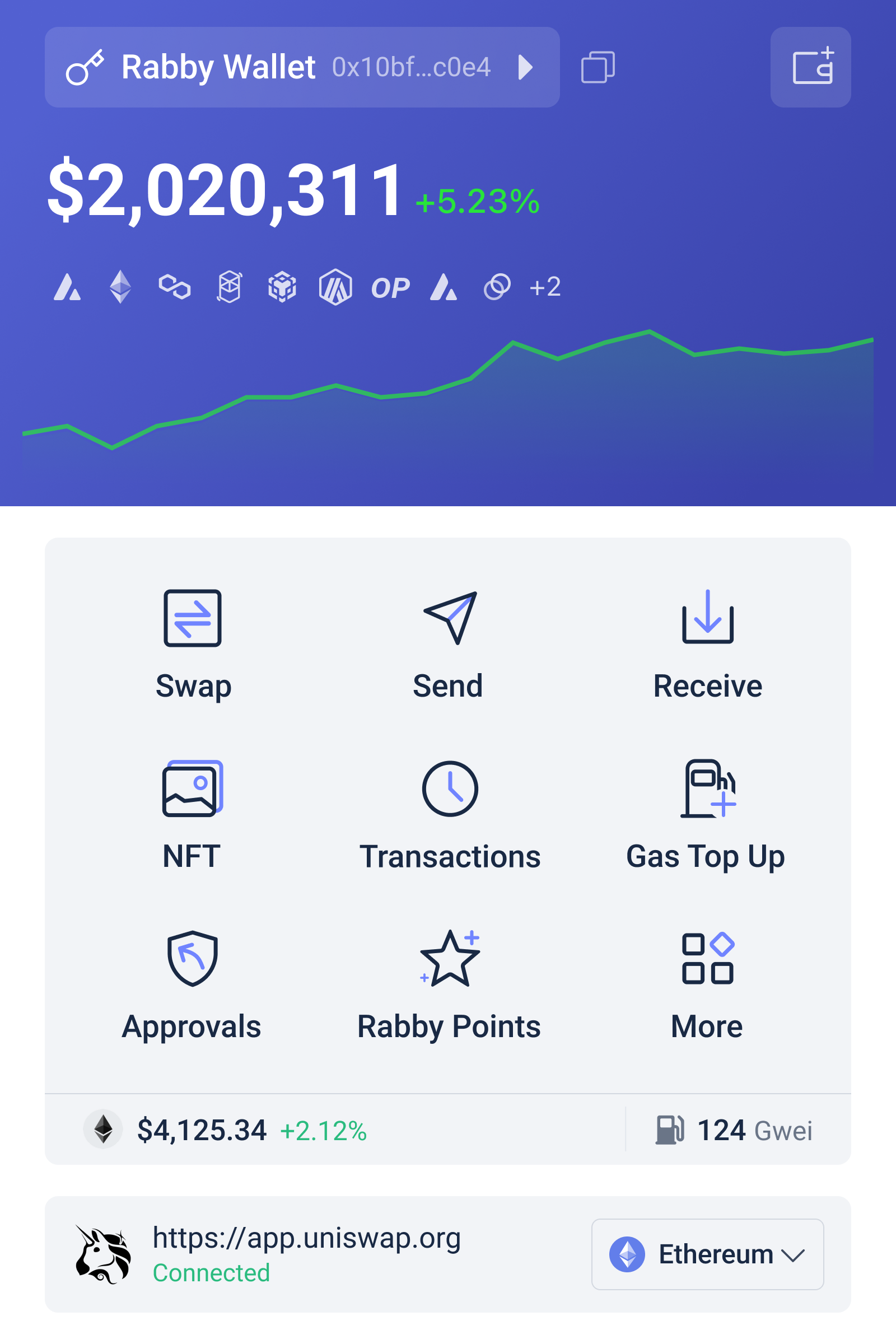

On the topic of wallets I recommend, I regularly tell friends about solutions that blend security and usability. One tool that stands out combines transaction simulation, multi-chain portfolio tracking, and strong permission management in a crisp UI. If you’re exploring options, check this out—rabby wallet—it’s the one I keep coming back to when I want simulations and clear approval controls. There, I said it; I’m biased because it solved a recurring problem for me. That said, no single product is perfect for every use case.

Here’s the thing.

Integrations matter much more than flashy design. A wallet that talks directly to major DEXs, bridges, and hardware devices without forcing weird workarounds wins. My experience in DeFi taught me that composability should be a convenience, not a headache. That means clear fallback behavior when a chain is congested and sensible defaults for approvals and slippage. Users benefit when the wallet authors think in terms of developer ecosystems, not just the UI.

Whoa!

Transaction simulation deserves another spotlight. Simulation isn’t just “will my swap succeed?”—it predicts slippage, front-running risk, and even subtle approval flows that can drain assets. I once watched a marginal trade turn into a sandwich attack in minutes; it was ugly and avoidable. Wallets that simulate and then explain the attack vector in plain English empower users. Not everyone will read the details, but having accessible warnings matters to less-experienced traders.

Okay, so—

Permission management is underrated. Users routinely approve infinite allowances without thinking twice. This part bugs me. Wallets that provide one-click revocation and limit approvals by default help reduce long-term exposure. It’s like locking your car—small habit, big defense. Also, showing when contracts were last used and by whom (if available) gives extra context that can prevent mistakes.

Wow!

Cross-chain portfolio tracking introduces unique UX puzzles. For instance, how do you show bridged tokens without double-counting them? There are tradeoffs between naive aggregation and analytic correctness. A smart wallet should allow toggles: show raw chain balances or normalized portfolio value. Initially I thought the raw view was enough, but then realized many users just want a clean net worth snapshot for taxes or personal tracking. So give both options and make them easy to switch.

Seriously?

Yes—bridging needs clear cost breakdowns. People often forget that bridging isn’t free; relayers, gas, and potential slippage add up. Presenting expected final amounts, along with worst-case and best-case estimates, builds trust. I like when wallets simulate the entire bridging flow end-to-end rather than assuming the bridge will behave perfectly. Those extra steps reduce surprises and build user confidence.

Hmm…

Let’s talk about advanced users for a moment. Power users want scripting, batch transactions, and custom gas strategies. They also want guardrails—automation doesn’t mean autopilot without brakes. Smart wallets offer “expert modes” that expose deeper controls but keep sensible defaults for normal folks. And sometimes power features should be gated behind confirmations, because mistakes at scale are expensive. I’m not 100% sure how to design the perfect expert UX, but gradual exposure seems promising.

Here’s the thing.

Legal and UX requirements intersect more than you’d think. In the US, tax reporting and KYC contexts push certain UX patterns—clear transaction history, exportable CSVs, and metadata tagging. Wallets that make bookkeeping easier reduce friction for real-world adoption. I often tell startups that if you remove administrative headaches, users will stick around longer. Small conveniences compound over time into real retention advantages.

Wow!

Privacy remains a complicated axis. Aggregating a portfolio across chains is helpful, but it also centralizes info on activity that some users prefer to keep private. Balancing convenience with privacy-preserving features (like local-only portfolio computation or optional pseudonymous modes) should be a priority. There are tradeoffs: more privacy can mean less convenience in recovery scenarios. For many people, that tradeoff is acceptable—but they should have the choice.

Okay, check this out—

Designing for real-world mistakes changes priorities. I once saw a friend paste the wrong address because the dApp autofilled clipboard data. Simple prevention like address labels, checksum validation, and rich recipient previews would have stopped the loss. Wallets that assume user error and design accordingly are more likely to retain users long term. It’s a small empathetic design principle that yields outsized security improvements.

Whoa!

Developers building dApps also benefit when wallets offer robust APIs. If a wallet can surface simulation results or risk warnings to a dApp (with user consent), then both parties can create safer experiences together. That composability creates an ecosystem effect where safety becomes a shared responsibility. I like solutions where dApps and wallets collaborate on user education, not where they compete for attention.

Hmm…

Finally, pockets of regulation will shape wallet features. Not all of that will be fun. But the smarter wallet teams will prioritize transparent controls and clear consent. People respond better when rules are explained plainly, not buried in legalese. That human-first communication reduces friction and builds trust in chaotic markets. And trust, at the end of the day, is the most valuable crypto-native product.

Where to Start (and What to Try Next)

Here’s the thing. If you’re choosing a wallet today, look for three practical things: accurate cross-chain portfolio views, transaction simulation with plain-English explanations, and granular permission controls you can manage from one place. Try small test transactions first to validate a wallet’s estimations. I’m biased toward tools that encourage safe behavior by default rather than relying on user vigilance. Experiment responsibly and keep backups—seed phrases still matter more than UI polish.

FAQ

Do transaction simulators actually prevent losses?

They reduce risk because they reveal execution details before you confirm, which helps catch suspicious approvals and mispriced trades; they’re not foolproof, but paired with permission management they make a big difference.

How does one wallet manage multiple chains securely?

By keeping keys local, offering hardware-wallet integration, and implementing clear guardrails for cross-chain actions; the UX around recovery and revocation is equally important, and good wallets prioritize those flows.